Tornado Destruction: Banks Bear Great Responsibility

Much is being written about local, state, and federal government responsibility for the destruction left in the wake of the tragic and historic tornado that hit St. Louis. Redlining and other racist public policies played a large part in creating the conditions that led to so many buildings collapsing. Most of those federal policies were overturned decades ago, but that didn’t end racist government interventions. After federal policies changed, local government continued to pursue racist policy in the form of an “urban triage” planning system that has become largely normalized.

While needed reparative policies have not followed the end of official redlining and urban triage continues, the idea that the government bears all of the responsibility for the ongoing lack of investment in majority-Black neighborhoods mainly helps provide cover for the actors that have continued to deny capital to potential homebuyers and small business owners, long after government policy changed. The truth is that most loan denials aren’t made by the government. They’re made by banks and other private lenders. These institutions deserve their fair share of public recognition for their culpability in creating the preconditions that led to this tragedy.

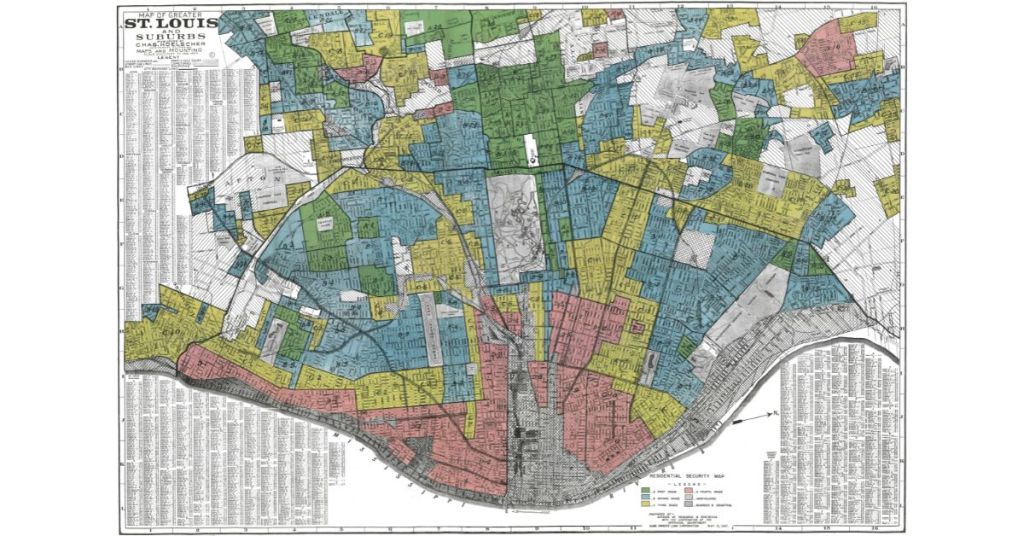

After federal “redlining” was retired to history’s dustbin, a private system designed to deny access to capital replaced the public system. The areas that were actually “redlined” by the Home Ownership Loan Corporation, which was a federal entity, make up a fraction of north city. This means that the area where lending has been cut off has only grown in the years after the federal government stopped its policy. In this new system, banks and appraisal professionals have set up rules that will almost always deny capital to people in majority-Black areas. The government is largely uninvolved. Decades of undervaluing property in majority-Black neighborhoods has become the reason capital is continually denied in these neighborhoods. It is an especially cruel example of the “chicken and the egg problem”. The result is that community development is racialized. As property values are so tightly tied to race, neighborhood redevelopment and demographic change remain tightly entwined in the form of gentrification’s displacement of minorities. This is true in cities across the country.

Even if everyone in a potential transaction is working in good faith and would like to make these loans, lender underwriting guidelines often result in the denial of lending in majority-Black neighborhoods. This is true even when the borrower’s ability to repay isn’t in question. This creates a moribund real estate market and keeps values low. This is despite federal policy officially encouraging banks to lend in underserved areas. While the Community Reinvestment Act (CRA) was put into place to prompt increased lending in these areas, it is not set up to force major shifts in lending activity. Instead, the law is designed to slowly ratchet up the floor of lending in low-to-moderate income areas. As we can all see, it has done so at a pace that is insufficient to overcome the inertia of our racialized real estate market. Even lenders who take their CRA obligations with the utmost seriousness only do a limited amount of lending in these areas, due to the real estate valuation system being designed in a way that makes denial the default decision. All the while, these same institutions have been profiting off of St. Louis’s Black community.

This lack of access to private lending has largely barred north St. Louis residents from the financial resources needed to stabilize homes and develop businesses. The situation demands homeowners on the northside finance major maintenance costs with cash. This is something that most white homeowners aren’t asked to do. Homeowners in majority-white neighborhoods can access home equity loans and other credit products that allow them to pay off major expenses over time. This makes upkeep costs far more manageable. People are right to be mad that the northside has been systematically deprived of economic development, but laying all responsibility at the feet of the public sector loses sight of the fact that our capitalist system is based on the profit motive. Racism is big business, and there are people who made a lot of money off of the denial of resources that led to so many houses collapsing. For instance, many banks provide lines of credit to payday lenders and other predatory industries that mainly exist due to the banks’ own poor history in communities of color.

As many have already pointed out, even if the Rams settlement monies were all spent on the recovery, it would represent a fraction of the capital needed for reconstruction. While FEMA will hopefully provide some support for displaced families, the agency doesn’t fully replace uninsured homes, of which there were many. Any realistic plan to rebuild will have to bring large amounts of private capital to the table, and it will take significantly more than the token amounts currently being offered by regional business leaders. If plans are made that rely almost entirely on public sources, those plans are guaranteed to fail. As such, it is important that we point out that the government was not alone in creating these conditions. The banks were active partners, and lenders should pay up. Without major contributions from the private sector, a northside diaspora is almost guaranteed. In light of this, justice-seeking St. Louisans would be well served to remember Willie Sutton’s famous, though apocryphal, answer to why he chose to rob banks: that’s where the money is.

Demanding that the government put money on the table to make up for its role in creating the conditions that led to this moment is a righteous call to action. To actually rebuild, it will need to be coupled with an equally righteous call for lenders to compensate the communities that they continue to starve for resources. The city government can’t heal this wound on its own. Even if granted, FEMA support will be insufficient to rebuild from the immense destruction to areas where many didn’t have homeowners insurance. Meanwhile, the private sector continues to profit from racism. Only if public and private actors both accept their roles in creating the preconditions for this tragedy, and work together in concert, will even a fraction of the damage be undone.

It is easy to take aim at the government, as the narrative is pre-built and already part of our civic conversations. It’s not wrong, either. That said, a narrow focus on the government’s well-documented role is convenient but provides cover for business interests, who continue to play a major role in starving the northside of resources. The banks have played an important and enduring role in planting the seeds of destruction that the tornado brought to fruit. They deserve their fair share of the blame and should play a major role in funding the private sector’s contribution to reconstruction.