Taxation Districts Show Changes In Regional Retail Spending Patterns

In recent decades, Community Improvement Districts and Transportation Development Districts have proliferated across the state of Missouri. The St. Louis region has been a hotspot of their usage. These taxation districts can be set up to levy sales, property taxes, or both. The most common version of both districts are set up in retail shopping/dining areas, where an extra sales tax levy is used to fund improvements, promotional staff for the district, and, very often, extra security for the district. The way they work is that a new taxation district, not unlike a school or ambulance district, is set up, after following state law and a vote of those in the district. Once these districts are set up, the tax revenues go into accounts that are administered by a district board. These boards often include prominent business people from within the district and also developer representatives, especially in the case of a “single site” CID/TDD, which is largely used to pay down debt taken on for development costs. In the city, the Board of Aldermen put the new taxation district to a vote of residents and property owners in the proposed district. In the case of CIDs related to individual development financing, the only real entities with a say are the Board and the property owner, who get to cast the sole vote in the election. For districts that encompass a commercial strip, residents and property owners in the footprint cast the deciding ballots.

Many of these districts don’t raise huge amounts of cash. They are often able to support one or two paid staffers and promotional materials for festivals, large sales events, etc. that occur in the district. On the other hand, some districts raise significant monies and can afford to spend heavily on promoting and securing their shopping corridors. There also are a lot of “single site” CIDs and TDDs. These are usually connected to a single business and don’t tell you much about larger trends in commerce. For this article, we tried to focus on districts that encompass multiple buildings or at least multiple businesses.

While there are often questions about the fairly opaque manner by which these taxation districts decide on their spending, we are not so much looking at this data for accountability. Rather, we’re looking at these districts as a way to see how the various districts are doing and if certain parts of town are overtaking others as retail sales leaders. By seeing how districts’ taxable sales numbers shift, relative to each other, one can get an idea about where our region’s shoppers are choosing to spend their money. Through this retail tracking lens, we consider changes in consumer behavior.

After reviewing Missouri Department of Revenue data, we have separated out the Missouri side of our region’s CIDs/TDDs into a few groupings:

- Central Corridor and North St. Louis

- South St. Louis

- St. Louis County

- St. Charles County

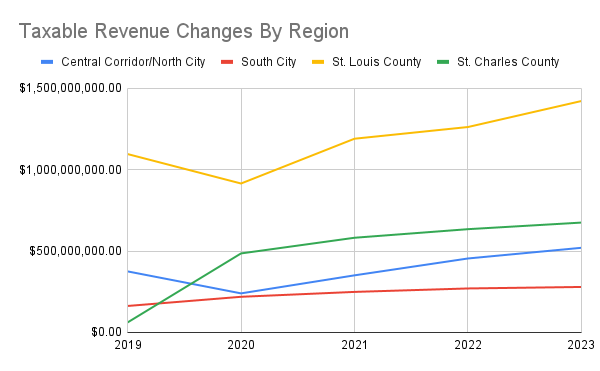

By splitting the CIDs/TDDs into subregions, readers should be able to see changes both within areas of the larger St. Louis region and between these sub-regions. To assist in seeing these intra-regional shifts, we’ve also produced a graph showing how the regions are performing relative to each other.

Central Corridor and North St. Louis

First, we look at the districts in the city’s central and northern neighborhoods. There are few of these taxation districts in north city. Downtown CID is obviously the long-time heavyweight in Central Corridor CIDs, with significant taxable sales revenue that supports staffing and significant security contracting. Despite the central business district’s well-publicized struggles, taxable sales in the CID continue to climb. Even in a down year for the Cardinals, downtown and Ballpark Village both continued to increase sales, though Ballpark Village’s growth rate has slowed. At about half of the taxable sales of Downtown CID, the Central West End CID and the Loop Trolley TDD are also districts with significant taxable sales. As readers probably know, the Loop Trolley TDD was started in the hopes of subsidizing the eponymous trolley line. While the trolley has not been very successful, these taxable sales are put toward the line’s limited schedule. The revenue from the Central West End CID taxable sales is likely going toward more traditional usages (promotion, security, etc.) for these districts. Readers will note that the next taxable sales tier shows that The Grove and Ballpark Village CIDs generate similar amounts. Also in this tier is the new City Foundry CID, which has eclipsed the taxable sales of Ballpark Village, while taxable sales in The Grove remain slightly higher. This really shows the success of the new Midtown shopping and dining complex.

At the low end of the spectrum, we can see that Laclede Landing’s taxable sales numbers have been declining. The same is true for the Tucker and Cass CID, where Paul McKee’s gas station and now-shuttered grocery store are located. It is important to note these are in raw dollar terms, so a district whose taxable sales have stayed flat or declined has likely seen a decent drop in commercial activity, given recent years’ heightened inflation.

South St. Louis CIDs

As you will see in the chart below, south city has a bevy of CIDs. Within these CIDs are a number of strip malls, such as the Loughborough Commons and Southtowne CIDs. The South Grand CID covers the bulk of the commercial district, but it excludes the Schnucks. On the other hand, the Cherokee CID includes the Save A Lot store that is located just south of the commercial district. The data shows that the Cherokee CID has surpassed the South Grand CID’s taxable sales numbers. Rising grocery prices are a lift to the Cherokee CID, as South Grand’s doesn’t have a big store to anchor it. We can also see that the newer Soulard CID has been bringing in a lot of taxable sales. In a short time, it has already exceeded Loughborough Commons’ taxable sales numbers. The far-south shopping center has faced numerous store closures, alongside the national decline in spending at home improvement stores, like the Lowe’s located in the center. On the other hand, increasing food prices at Schnucks somewhat offset these losses.

St. Louis County: Where TDDs Reign Supreme

When looking over tax districts in St. Louis County, it is quickly apparent that the TDDs in major suburban shopping areas generate far more taxable sales, when compared to their CID cousins. Most notably, the Chesterfield Valley TDD is on pace to exceed $1 billion in annual taxable sales. It simply dwarfs every other CID/TDD in the region. To put this in perspective, you’ll see that the Town & Country Crossing TDD’s taxable sales is a fraction of the Chesterfield TDD’s annual haul.The smaller of the two suburban shopping districts’ TDDs brings in roughly the same amount as the city’s Downtown CID. It really drives home how much of the region’s commerce has moved to the Chesterfield Valley. As the chart below shows, none of the county’s CIDs come anywhere close to the taxable sales generated by these two TDDs. There are multiple CIDs in the Brentwood shopping area. For the sake of not cluttering the graphs, we chose the largest of the districts, leaving smaller ones aside. Similarly, we only showed one Westport-area CID, though there are multiple districts in that area.

St. Charles County

Lastly is St. Charles County, which doesn’t yet have a ton of shopping districts that have CIDs. One notable part of this last graphic is the sheer size of the new Wentzville CID. If you had any doubt about Wentzville’s breakneck rate of growth, the fact that its new CID is already bringing in multiples of the Downtown CID’s taxable sales should help provide context on the speed of the development in what was once a largely rural part of St. Charles County. In fact, it is basically the only CID that seems to be in any way preparing to give the Chesterfield Valley TDD competition for most taxable sales. That being said, it would have a lot of ground to make up, and Chesterfield TDD’s continued retail growth will likely mean that it remains the leader for many years to come.

Changes In Taxable Sales Show Trends In Commercial Spending

These shifts in spending give us an idea of where consumers are going to shop, dine, and attend various entertainment events. Looking at these numbers, we see that places like City Foundry and Chesterfield’s burgeoning retail and entertainment scene have been drawing major crowds, while places like South Grand and north county’s Plaza on the Boulevard shopping center have seen revenues basically holding steady. Given the inflationary environment in which these sales happened, just holding steady actually indicates a slight decline in spending. Some places, like Laclede’s Landing, show that new investment has failed to turn the page on commercial decline. To the west, St. Charles County boasts fewer special taxation districts, but the new Wentzville CID is already one of the biggest in the state.

As readers can see, the big winner recent changes in spending habits have benefitted St. Louis County, St. Charles County, and the City’s Central Corridor. Meanwhile, spending at South City CIDs has leveled out. Given the inflationary environment, this is a concern for retailers in these southern CIDs. Chesterfield and City Foundry have driven increased spending along the I-64 corridor. St. Charles County should expect to see continued growth, as Wentzville is a rapidly expanding area, which should mean more taxable sales in this region. All in all, these special taxation districts remain a popular way for developers and governments to raise more revenue for projects and districts that they hope to grow.

Author’s note: Multiple taxation districts were contacted for comments. After over a week, none have responded. If comments are submitted after publication, they will be added to this piece.